Hello all, and welcome to Market Fantasy. To recap the last

few weeks’ episodes, so far we have created a market index of fantasy players –

the FOW. This has been tracked mostly weekly. Then, after a short history of

the Dow Jones Industrial Index, we kicked out two players from the original FOW—out

with Albert Pujols and Ryan Braun and in with Chris Davis and Carlos Gonzalez.

After that, I got an adorable Keeshond puppy named Ash so the updates came less

frequently causing the tens of people that read this blog to go into serious

panic withdrawal, I’m sure.

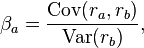

Well, I’m back now. Today’s blog post is kind of the reason I started this blog in the first place. I wanted to take a look at Beta in terms of fantasy sports players. Besides being Sony’s first failed attempt at dominating a media format, in investing terms, Beta measures systematic risk based on how returns co-move with the overall market. Got it? What that means in plain English is that Beta measures the swing in returns of a stock compared to the swing in returns of an index. The index in question is usually the S&P. To calculate Beta, we take the covariance of rates of return of the stock and rates of return of the index. This is divided by the variance of the rate of return of the index. The formula is as follows:

This calculation will give us a number. This number is the

Beta of the stock. So what does this number mean, other than that you can do

advanced calculations correctly? Like I said above, this number measures the

volatility of an asset compared to the index. But what does that mean? The

following chart from Wikipedia will help decipher Beta:

Value

of Beta

|

Interpretation

|

Example

|

β < 0

|

Asset generally moves in the opposite

direction as compared to the index

|

An inverse exchange-traded fund or a

short position

|

β = 0

|

Movement of the asset is uncorrelated

with the movement of the benchmark

|

Fixed-yield asset, whose growth is

unrelated to the movement of the stock market

|

0 < β < 1

|

Movement of the asset is generally in

the same direction as, but less than the movement of the benchmark

|

Stable, "staple" stock such

as a company that makes soap. Moves in the same direction as the market at

large, but less susceptible to day-to-day fluctuation.

|

β = 1

|

Movement of the asset is generally in

the same direction as and about the same amount as the movement of the

benchmark

|

A representative stock, or a stock

that is a strong contributor to the index itself.

|

β > 1

|

Movement of the asset is generally in

the same direction as but more than the movement of the benchmark

|

Volatile stock, such as a tech stock,

or stocks which are very strongly influenced by day-to-day market news.

|

At this point, I’m sure most of you are thinking “Alright

nerd, enough math, how does this help me in my fantasy league brosephus?” Well,

let me tell you. As stated above, Beta is a measure of volatility. The way this

relates to fantasy sports is to try to find the players with Betas that match

your style. You can identify consistent performers week in and week out with

this formula. If you want to cut out some risk on your team, try to go after

players whose Beta is close to one. These are players who will be the most

likely to perform on a consistent level. Conversely, if you’re a gambler, maybe

a player with a high Beta is more up your alley. These are the feast and famine

players you can ride to glory one week and who will flush your team straight

down the toilet the next.

This can be very helpful when constructing your roster. Use

players whose Beta is close to one to offset players with higher or lower

Betas. Fantasy managers do this all the time when constructing their fake

rosters for individual stats (holding Adam Dunn for HR? you better have a safe

batting average guy like Mauer to offset Dunn’s BA torpedo), why not broaden

that strategy to include overall performance? Portfolio managers look at a

stock’s Beta, so why not use it to construct your imaginary dynasty? With that

in mind, here are some position-by-position examples of consistent and extreme

Beta cases. Note, some players are listed in a different position than their

natural position, but they are eligible there in most leagues.

Catcher:

Value

of Beta

|

Player

|

Beta

|

||||

β < 0

|

|

|

||||

β = 0

|

||||||

0 < β < 1

|

||||||

β = 1

|

||||||

β > 1

|

1st Base

Value

of Beta

|

Player

|

Beta

|

β < 0

|

Carter, Chris HOU

Carpenter, Matt STL

|

-0.40

-0.23

|

β = 0

|

Votto, Joey CIN

|

0.00

|

0 < β < 1

|

Freeman, Freddie ATL

Dunn, Adam CHW

|

0.23

0.51

|

β = 1

|

||

β > 1

|

2nd Base

Value

of Beta

|

Player

|

Beta

|

||||

β < 0

|

|

|

||||

β = 0

|

Gonzalez, Marwin HOU

|

0.00

|

||||

0 < β < 1

|

Murphy, Daniel NYM

Kipnis, Jason CLE

|

0.22

0.47

|

||||

β = 1

|

||||||

β > 1

|

3rd Base

Value

of Beta

|

Player

|

Beta

|

β < 0

|

Longoria, Evan TB

Machado, Manny BAL

|

-0.48

-0.14

|

β = 0

|

Encarnacion, Edwin TOR

|

0.00

|

0 < β < 1

|

Dominguez, Matt HOU

Alvarez, Pedro PIT

|

0.36

0.49

|

β = 1

|

||

β > 1

|

Shortstop

Value

of Beta

|

Player

|

Beta

|

β < 0

|

Cozart, Zack CIN

Cabrera, Asdrubal CLE

|

-0.61

-0.35

|

β = 0

|

Escobar, Yunel TB

|

0.00

|

0 < β < 1

|

Ramirez, Alexei CHW

Aybar, Erick LAA

|

0.08

0.65

|

β = 1

|

||

β > 1

|

Outfield

Value

of Beta

|

Player

|

Beta

|

β < 0

|

Choo, Shin-Soo CIN

Holliday, Matt STL

|

-0.45

-0.41

|

β = 0

|

Eaton, Adam ARI

|

0.00

|

0 < β < 1

|

Bautista, Jose TOR

Werth, Jayson WAS

|

0.66

0.75

|

β = 1

|

||

β > 1

|

Pitcher

Value

of Beta

|

Player

|

Beta

|

||||||

β < 0

|

|

-0.85

|

||||||

β = 0

|

Alvarez, Henderson MIA

Chapman, Aroldis CIN

|

0.00

0.00

|

||||||

0 < β < 1

|

Scherzer, Max DET

Wilson, C.J. LAA

Rodney, Fernando TB

|

0.47

0.67

0.55

|

||||||

β = 1

|

Fernandez, Jose MIA

|

1.00

|

||||||

β > 1

|

|

|

So there you have it. Unfortunately there weren’t any

hitters with Betas over 1, but there were pitchers with Betas all over. As we

learned about Beta, negative Beta and Beta over one can have similar effects in

that they are both more volatile, just moving in different directions.

Combining hitters with negative Betas (those who tend to have big swings in the

opposite direction as the index) with those Beta is closer to one (those who

tend to move closer to the index) can help you create a team of players that both

performs consistently while having enough upside to give you those big weeks.

So aim for zero? Did I get that correctly?

ReplyDeleteAlso your formula showed up blank for me

Zero means very consistent. You can use those type of players to offset players with a negative Beta who are more prone to ups and downs

ReplyDeleteBut over the course of a full roster 0 should field a competitive team?

ReplyDeleteGenerally yeah.

ReplyDeleteActually, I meant closer to one. Those are the ones that move with the index, which is made up of stars.

ReplyDeleteSo to expand, toy want to have a combination of one's and negatives. Since the ones move with the index, and the negatives opposite, they will act to cancel each other out and keep your team consistent

ReplyDelete